What is Financial Reconciliation? Definition, Process and Examples

What is Financial Reconciliation?

Financial reconciliation is defined as the process of tallying internal financial transactions and statements with external data sources. This data can be in the form of bank statements, vendor statements, customer statements etc.

The goal of financial reconciliation is to ensure that there are no discrepancies between internally maintained records and actual reality of company transactions and general ledger of the company. To achieve this, reconciliation takes place across all aspects of accounting and finance - accounts payable reconciliation with vendors, accounts receivable reconciliation with investments and customers, payroll reconciliation, bank reconciliation, and inter-company reconciliation among subsidiaries and business branches.

Key Steps in Financial Reconciliation

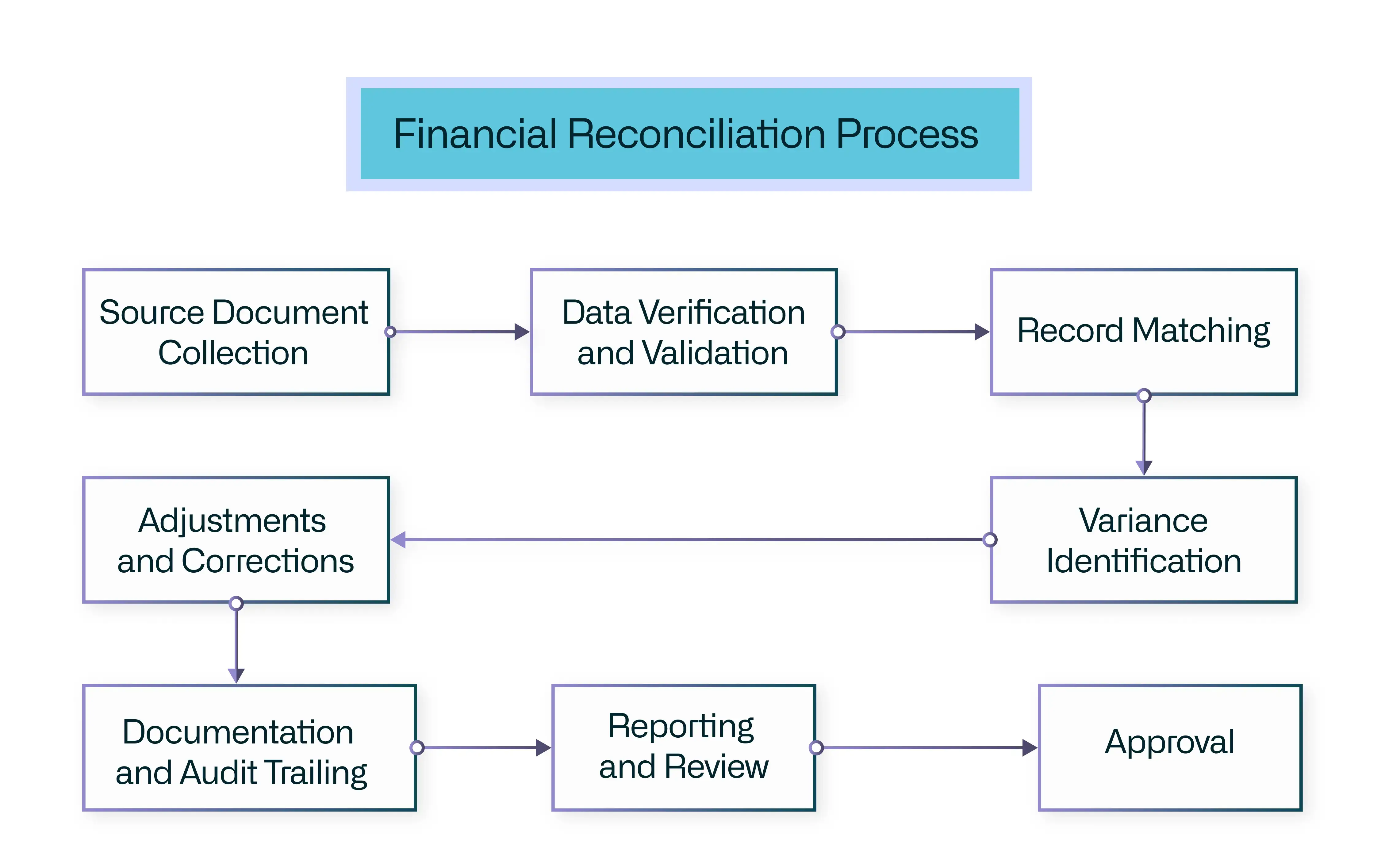

Financial reconciliation starts with data collection and ends with the final financial reporting. Here is how it unfolds in key steps:

- Step 1: Financial data collection

Financial data such as ledger reports, vendor invoices, goods received note (GRN), payroll data, sales data, company investment details, etc, are typically maintained in an enterprise resource planning (ERP) system. However, for smaller firms, this information may exist in silos such as in CRMs, accounting software, and HR management software etc.

- Step 2: Data validation process

The data collected is first validated for accuracy and completeness. In case of missing information, the accounting team may engage with team leads and employees for resolution.

- Step 3: Record matching process

Record matching is where the actual reconciliation takes place. At this stage the accounting team is matching the internal company data with external sources of truth, such as the company's bank statement and investment documents.

- Step 4: Variance identification

If any discrepancies arise between internal and external data, then these line items are sent for enquiry and resolutions. For example, these can be a mismatch in customer payment, pending vendor invoices, excess payouts etc.

Variances and discrepancies are handled through pre-set processes and protocols of enquiry and resolution. Based on the results, the balance sheets need to be corrected for the financial statements to reflect the truth.

- Step 5: Adjustments and corrections

Adjustments in the company's ledger report are made based on final reconciliation results. For example, there may be investment returns that were expected but not yet credited, customer payments that may be undergoing bank processing etc. All such situations need to be part of the financial report statement that is sent from the CFO’s desk.

In cases of any errors in calculations or estimations that surface, these numbers need to be corrected where required.

- Step 6: Reporting and review

The result of financial reconciliation is the final report which now reflects the current state of affairs in the company's balance sheet. This information plays a key role in cashflow forecasting and budgeting. After the report is published to the company's stakeholders and CEO, further steps may be taken to reduce errors and discrepancies that were found during the reconciliation process.

Related: What is Finance Automation?

Types of reconciliation under financial reconciliation

Financial reconciliation is a broad term that encompasses several smaller reconciliations. Whole these vary across organizations depending on internal structures and processes, here is a list of typical reconciliations that take place:

- Accounts payable reconciliation

Accounts payable reconciliation encompasses verification of any external outflow of cash from the company, be it to suppliers, rent payments, investments, dividend payouts, asset purchases etc. The process involves checking matching all such payments made with the company's bank statement and that the payments have been confirmed in the statements from recipients.

- Accounts receivable reconciliation

Account receivable reconciliation includes verification of all cash inflow to the company in the form of customer payments, refunds/ compensations, investment returns, asset sales etc. Here, all cash inflow data in the internal records are matched with bank statements and external records to ensure that the balance sheets are reflecting the accurate state of cash available to the company.

- Banking and credit reconciliation

Banking and credit reconciliation is done to ensure that expected lines of credit are available and open, that banking service charges are accurate and that no additional fees have been levied and that the bank account statements match the internal records of the company. During this process, companies also check for any stalled/ held up payments by the bank due to errors or processing issues. This helps clear out any banking bottlenecks that may have existed but overlooked.

- Payroll reconciliation

Payroll reconciliation is conducted to ensure that there are no excess, pending or duplicate payments made to employees and that HR documents on employee onboarding and exit are reflected correctly in the payroll system.

- Inter-company reconciliation

Inter-company reconciliation is key for any large enterprise with subsidiaries and branches. This process ensures any inter-company financial transactions such as purchases, debts, asset transfers etc, are all in the books and reflects accurately in shareholder reports and balance sheets.

Related: What is Expense Management Automation?

Importance of financial reconciliation for enterprises

Financial reconciliation is cornerstone for accurate financial reporting and staying ready for any external audits. Here are the key factors which makes this process so important:

- Confirms the company’s financial health

The primary goal of the elaborate and detailed nature of a financial reconciliation is to ensure that every transaction from the company’s account has the supporting document for validation. This ensures that the final result of the organization’s financial statement is an accurate reflection of the state of the company ledger and financial health.

- Identifies errors and lapses

The financial reconciliation process reveals any past errors that were wrongly logged, or any issues with the bank statements, vendor/ customer reports etc. The matching of the internal records with external data may reveal issues with the company’s own process or may even reveal issues with the vendor’s or customer’s books.

The result may require reassessment of employee training, better processes for collaboration between accounting and other departments, improved financial reporting practices etc.

- Keeps the books audit-ready

Being audit-ready requires a company to work like a self-cleaning engine. The goal is not for the auditor to expose issues in the company’s books, but rather to be in a state where no issues exist at any given time. For this to be the default state of the company’s accounting practices, regular financial reconciliation and air-tight accounting practices like 3 way matching, are cornerstone best practices processes.

- Ensures regulatory compliance of company transactions

Different geographies operate under different regulations, be it national, state or a group of nations like the EU. The company’s financial process already takes them into account, however, the degree to which they are being followed in daily practices is key to ensure compliance at any given time. The financial reconciliation process ensures that all set standards are being practiced and any lapses are reconciled.

Get Started

With Rever

- Automate finance operations.

- Rigorous authentication, continuous closure.

- Chat with your data with Agent.

- Get proactive decision Nudges.

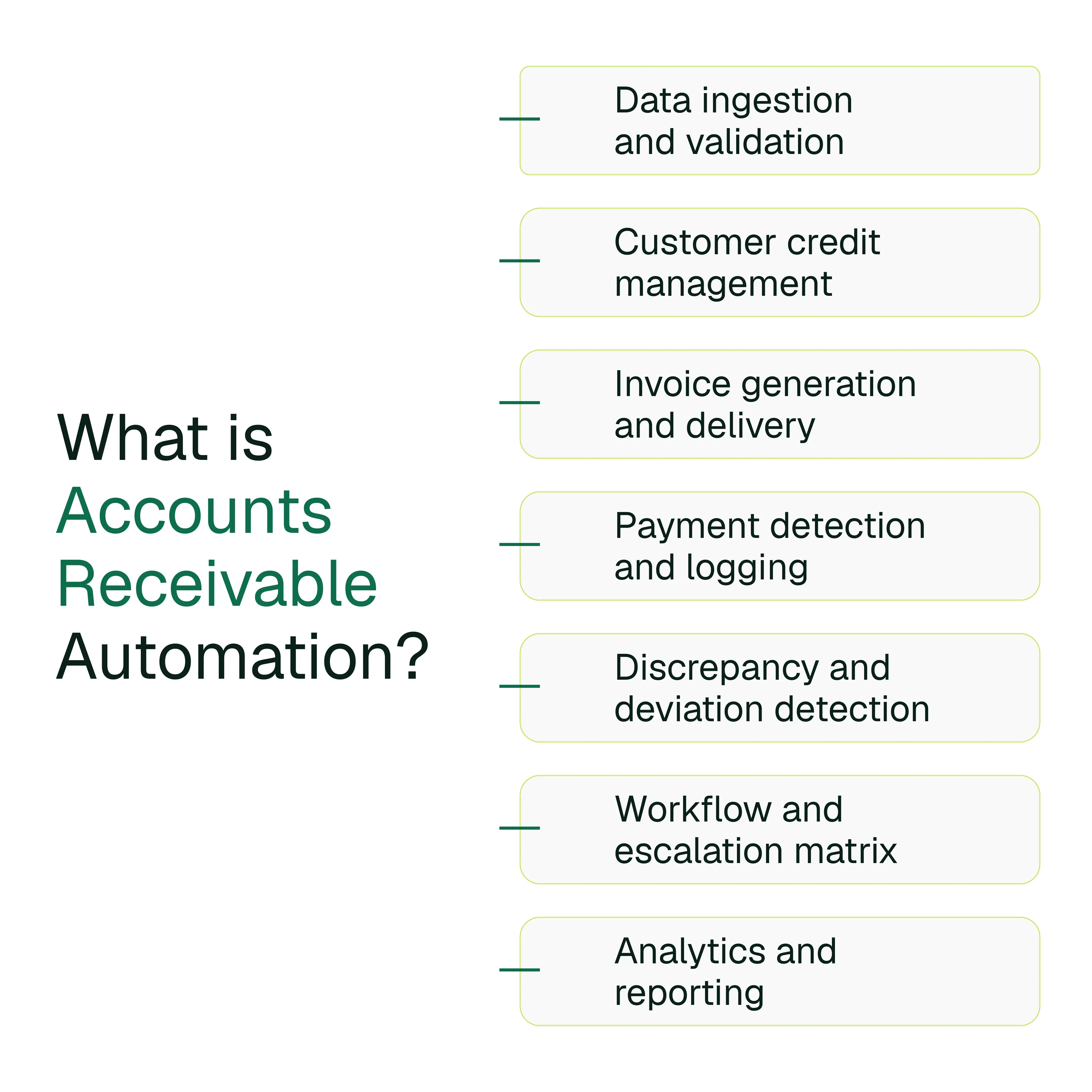

What is Accounts Receivable Automation? Process, Examples, Benefits and Best Practices

Accounts receivable automation is defined as the process of using computing technology to deliver complete or partial execution of data-intensive and repetitive tasks in the department. Examples of key areas of accounts receivable automation include customer credit checks, payment reminders, invoice generation, payment processing, reconciliations etc.

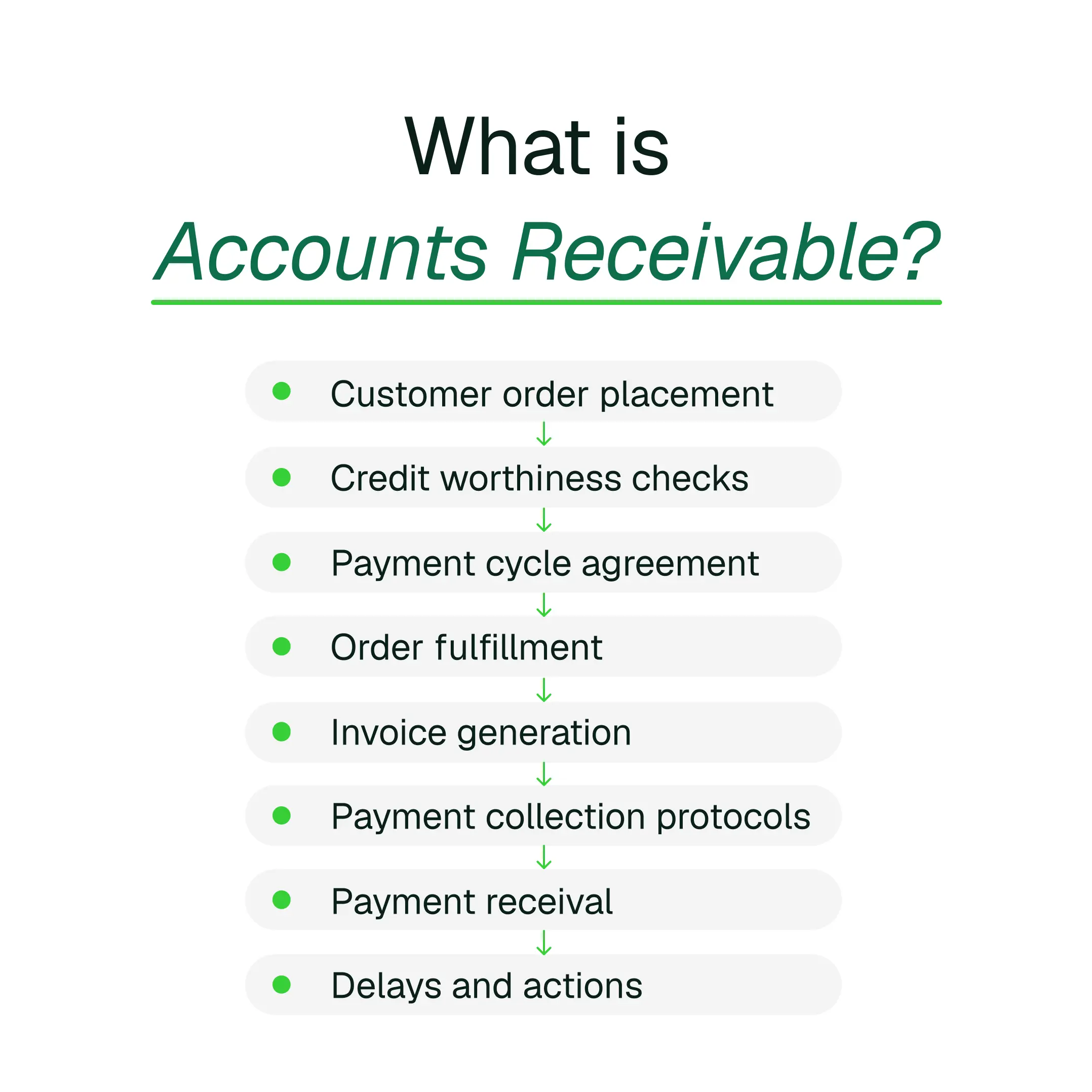

What is Accounts Receivable? Definition, Process, Examples and Best Practices

Accounts receivable for a business is defined as any due customer payments that are owed to the company in lieu of availed goods/ services. This system comes into effect where customers are allowed to purchase goods/ services on a credit basis.

What is Finance Automation? Definition, Components, Types and Best Practices

Finance automation is defined as the process of using software to perform certain financial tasks without requiring human intervention, within an organizational framework.