What is Accounts Receivable? Definition, Process, Examples and Best Practices

.png?prefix=hero)

What is Accounts Receivable?

Accounts receivable for a business is defined as any due customer payments that are owed to the company in lieu of availed goods/ services. This system comes into effect where customers are allowed to purchase goods/ services on a credit basis.

In finance operations, accounts receivable is classified as an ‘asset’, as it is expected to return cash, but in case the customer payment is not received within a stipulated time, it converts into a ‘debt’ in the company’s balance sheets.

Due payments classified as receivable by a business implies that this amount is expected clearance in the short term, typically within a month, but might be extended up to a year before it gets classified as a bad debt in the company balance sheets. Upon receival, the amount becomes part of the company’s actual revenue/ cashflow.

While a company is at discretion as to how long they want to classify a due amount as receivable, GAAP standards set a threshold of 1 year, after which a company should categorize it as a bad debt.

For example, a company posts $100,000 as accounts receivable for the month of April 2026. This means that the company is claiming to have sold this amount in goods/ services to customers in a post-paid system, and is awaiting payment, which is expected to be cleared in the short-term. Suppose $90,000 of this amount gets cleared, within the next month, then this amount gets reflected as revenue for May 2026 in their balance sheet. The remaining $10,000 still remains as receivable which is expected to be cleared soon.

In financial analysis, accounts receivable of a company plays a key role in projecting short-term cashflow, and assessing overall health of the business. Enterprise processes should be set up to ensure a smooth receivable to revenue cycle, and avoid customer payment delays or defaults which can add to company debt in the balance sheet.

Account Receivable Process: Key Components

- Step 1: Customer order placement

Accounts receivable comes into play as soon as the sales team finalizes a customer deal and the order is placed. The accounting team records this action and begins their work in checking if this order can be processed through credit or needs to be pre-paid. In smaller organizations this may be a simultaneous process alongside the deal closure.

- Step 2: Customer history and credit worthiness checks

The accounting team then follows protocols for checking customer history and credit worthiness. Depending on company policies, a new customer may or may not be qualified for credit lines. For renewals, depending on payment history, a post-paid monthly payment line may be set up on the basis of credit. Further checks involve looking at publicly available customer financial statements and health as metrics for assessment.

- Step 3: Payment cycle agreement

The customer and the supplying company then come to a formal agreement on how long the credit lines can run, how often they need to be cleared and potential liabilities the customer will incur in case of delays or default.

Once the documentation is complete, the deal moves to order fullfillment by the supplying company.

- Step 4: Order fulfillment and documentation

The company delivers the items as per agreement of sales and collects required documentation from the customer, such as delivery acknowledgement, including receipts of quality and quantity etc. These are key to ensure that there is sufficient proof that the order was delivered as per requirement and promises in the agreement.

- Step 5: Invoice generation

Upon completion of delivery, the company now generates an invoice and is sent to the customer using appropriate channels, typically, via email, to the purchase/ accounting team. This document may contain the expected date of payment as per the agreed upon payment cycle.

For publicly listed companies, this invoice value is placed in the financial statement as accounts receivable and sales, but not as cash flow, as the amount has not yet been received. This is however still used for future cash flow evaluation and estimation of net worth of the company.

- Step 6: Payment reminders and collections protocols

The supplying company’s accounts receivable team may send payment reminders as per collection protocols. In case of delays, further reminders and discussions may take place to extend the payment date.

- Step 7: Payment recieval and book closure

Once the payment is received from the customer, the amount is reflected as a revenue cashflow for the company and accounts receivable closes the book.

- Step 8: Payment delays and actions

In case of further payment delays, the company may explore legal avenues of action, and/ or may sell the account to collections agency for a fraction of the price, a process also known as accounts discounting. At this stage, the remaining amount becomes a debt and may be written off as a one time debt payment. This amount is deducted from the final cash flow in the company's financial books.

Importance of Accounts Receivable in Enterprises

- Ensuring sales to cashflow conversion

Sales is not cash realization until the customer payment is received in full, and till then is deemed as an asset that is expected to reap its equivalent amount in future. This is key to understanding the importance of an effective accounts receivable process that is responsible to ensure the proper conversion of product/ services sales to final cashflow that can become real operating capital for the company.

- Preventing sales assets from becoming liabilities

Accounts receivable in the form of sales is an asset, unless the customer payment is significantly delayed enough to be deemed as a payment default. In such a scenario, what was once an asset, is now a liability and is classified as debt. The accounting team, along with the sales and customer accounts management teams at large, have the key responsibility to ensure that such a situation does not arise through proper customer assessment and management of receivable assets.

- Increasing accuracy of financial projections and bolstering confidence

Investors, stakeholders and shareholders assess a company’s future cashflow through projections based on receivables on sales. When these receivables become realized after payments, they add to the accuracy of these projections, else they downplay the confidence in sales, and hence the company at large.

Proper management of accounts receivable plays a key role in achieving goals of cash realization and overall financial projections for the company, and thereby bolstering stakeholder, investor and shareholder confidence.

- Enhancing overall capital availability and business growth

Cash received from customers through sales is the key pillar of working capital, as well as securing future investment valuations. Typically, most big clients pay in the form of credit based on requirements and are settled through monthly accounts receivable closures. It plays directly into working capital availability for business operations, debt payments and overall growth of the company.

Best Practices for Managing Accounts Receivable in 2026

- Setting clear payment timelines in agreement

One of the key pillars of accounts receivable is timely and predictable cashflow is setting clear payment deadlines through signed agreements with customers at the time of deal closure itself. This ensures that both parties are fully aware of expected timelines, and consequences of delays.

- Digitization of enterprise operations

Digitization of the end-to-end accounting and enterprise operations is no longer a good-to-have, it's a must-have. This includes ensuring that all historic data is uploaded to self-hosted or cloud servers and that all new data is strictly digital-first.

This step is also key to any automation and AI capabilities, as the system will gather contextual information using this historic and current data.

- Automation and decision intelligence

Finance automation and AI capabilities of platforms such as Rever can help cut down closure time from days to hours, automatically send reminders to customers, provide real-time information from live data in your systems, perform automated record matching, detect and surface deep seated anomalies and trend deviations, and more.

Plus, contextual and role-based decision intelligence from Rever ensures that your receivables and finance team at large remains days ahead of deadlines, which goes beyond just insight dashboards that most teams rely on.

- Proper lines of internal and customer communication

The receivables team is in charge of ensuring that customer lines of communication and escalation are established and available. This is best done through an introduction at the sales closure phase, and then taking over communication after delivery.

Keeping all required stakeholders in the loop, especially in situations of escalation, should be part of the protocol and process. This also helps ensure that if leadership level help is required, there is proper context already documented.

What is Finance Automation? Definition, Components, Types and Best Practices

Finance automation is defined as the process of using software to perform certain financial tasks without requiring human intervention, within an organizational framework.

What is Expense Management Automation? Definition, Components and Best Practices

Expense management automation is defined as the process of using software to computerize enforcement of processes and policies related to employee expense benefits.

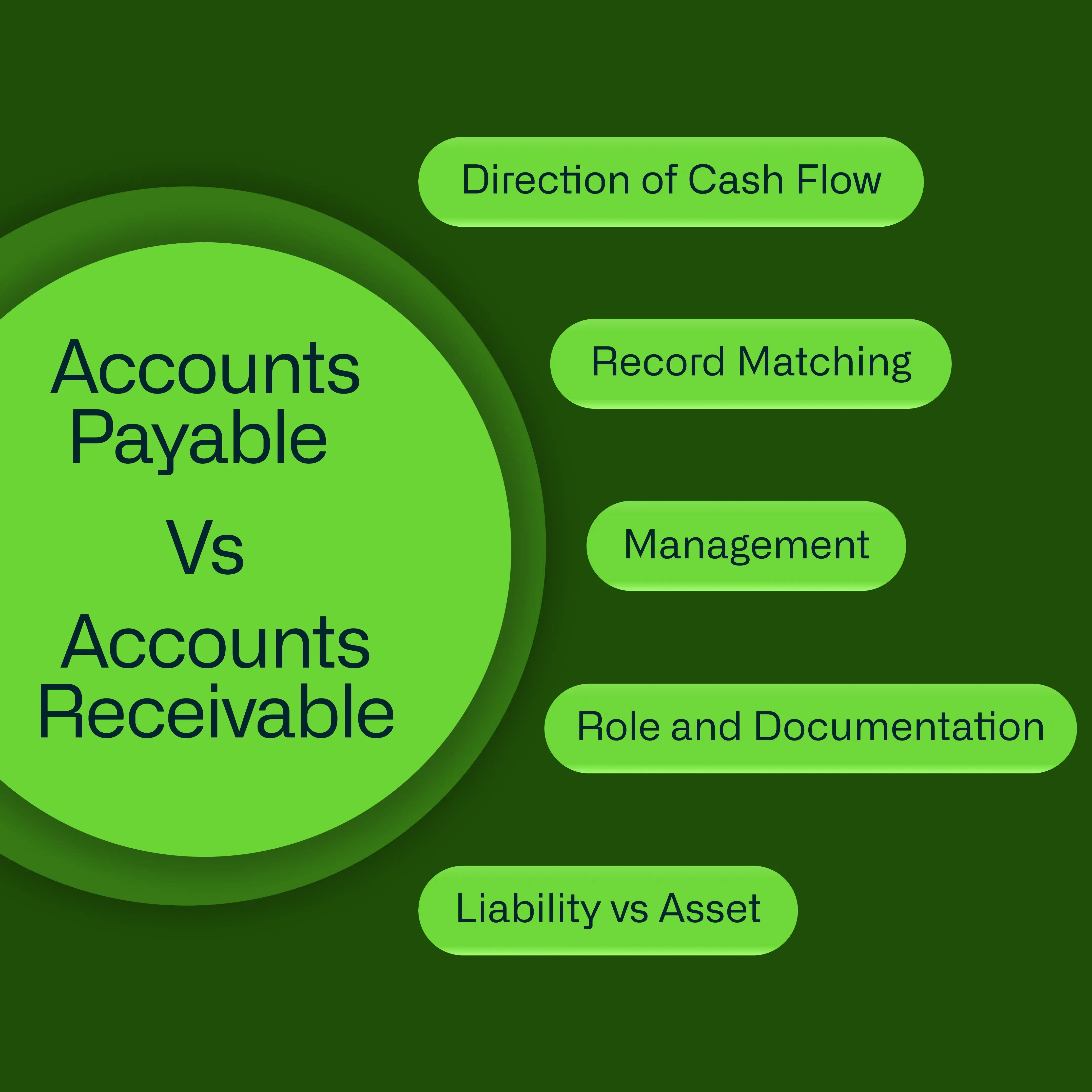

Accounts Payable vs Accounts Receivable: Key Differences and Similarities

Accounts payable and accounts receivable are two core pillars of enterprise accounting. Understand the key differences and similarities between the two.