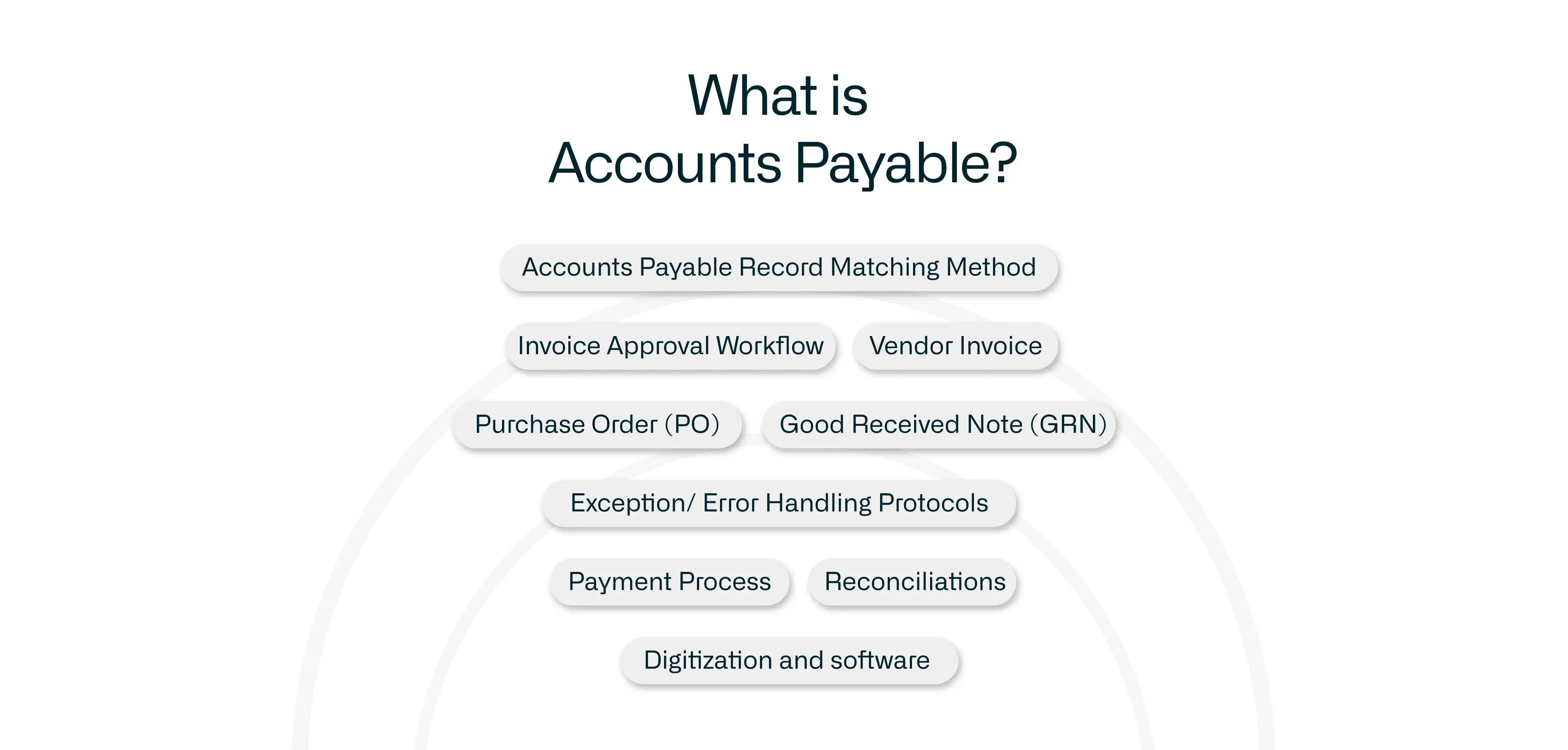

What is Accounts Payable?

Accounts payable is defined as an enterprise representation of money owed to vendors/ suppliers in the form of invoice claims with the company.

Inherently, accounts payable is a post-paid process, which are the current liabilities of the company. It does not include pre-paid services, which fall under current assets.

For example, if a design agency provides services to the product engineering team within a software company, it would typically be done in a post-paid format. The agency would provide the services and raise a monthly invoice to the firm, which would be received as accounts payable. This invoice is then verified, validated and cleared, based on internal accounts payable processes.

Accounts payable is distinguished from accounts receivable by a full reversal. Accounts receivable is the money owed by customers to the company for providing services/ products. Whereas for accounts payable, it is the money the company owes to its vendors/ suppliers. Notice that what is receivable for one enterprise, is payable for the other.

Related: Accounts Payable Vs Accounts Receivable - Key Comparisons

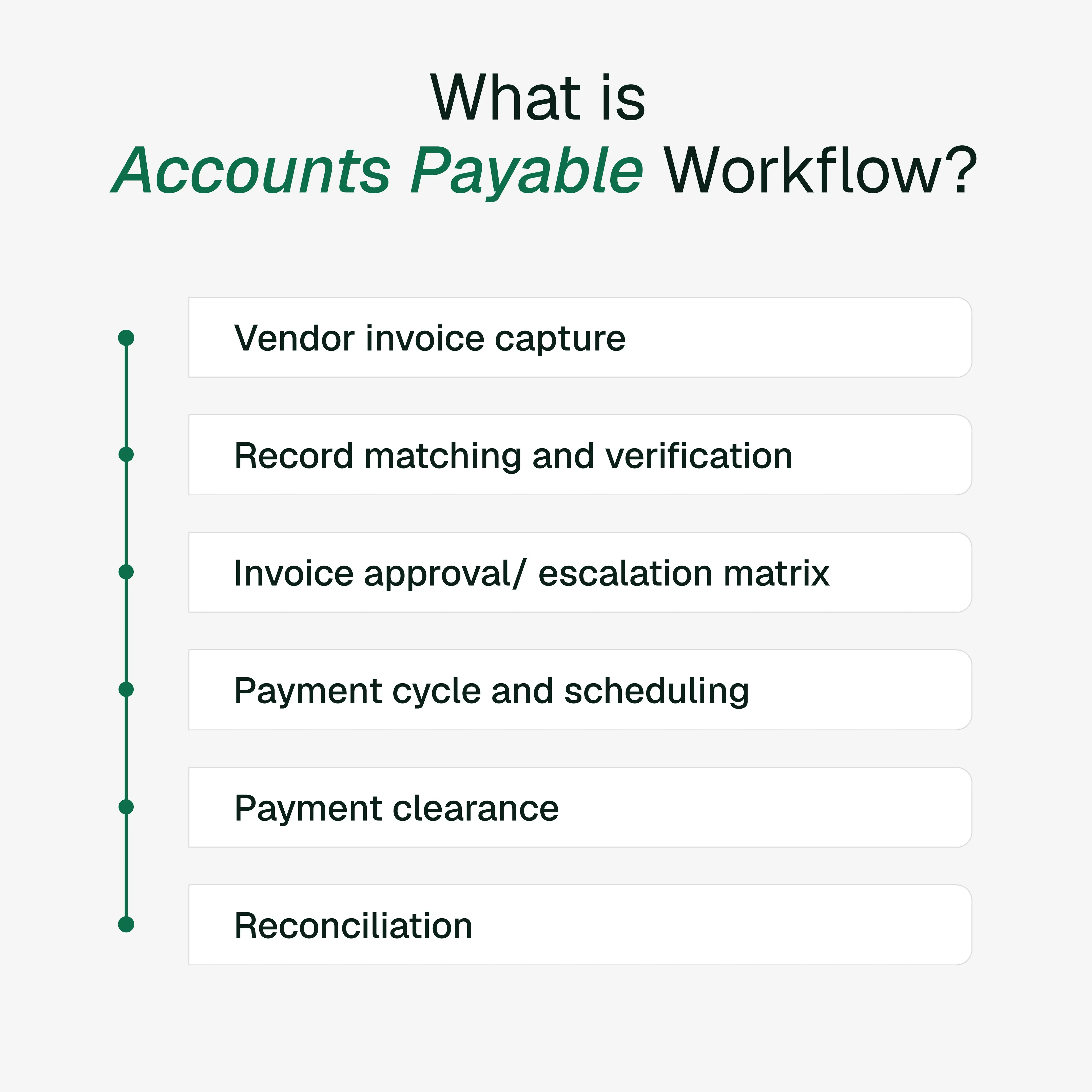

Key Components of Accounts Payable Process with Examples

Standard accounts payable workflow in businesses encompass several key process components required to ensure error-free, data-backed and audit-ready accounts book-keeping. A proper process is also key to ensuring timely and accurate vendor payments and enterprise supply-chain efficiency.

Here are the key components for an effective accounts payable process:

- Accounts payable record matching method

The cornerstone of effective accounts payable processing is the record matching methodology to be used for tallying vendor invoices with internal documentation to validate the invoice’s authenticity and accuracy. Typically, a 2 way match or a 3 way match is standard across industries.

In a 2 way match, the vendor invoice is matched against the purchase order (PO), and in a 3 way match, the additional documentation used is a goods received note (GRN) alongside the PO.

In very exceptional cases there may be a requirement for a 4 way match which includes an investigation report.

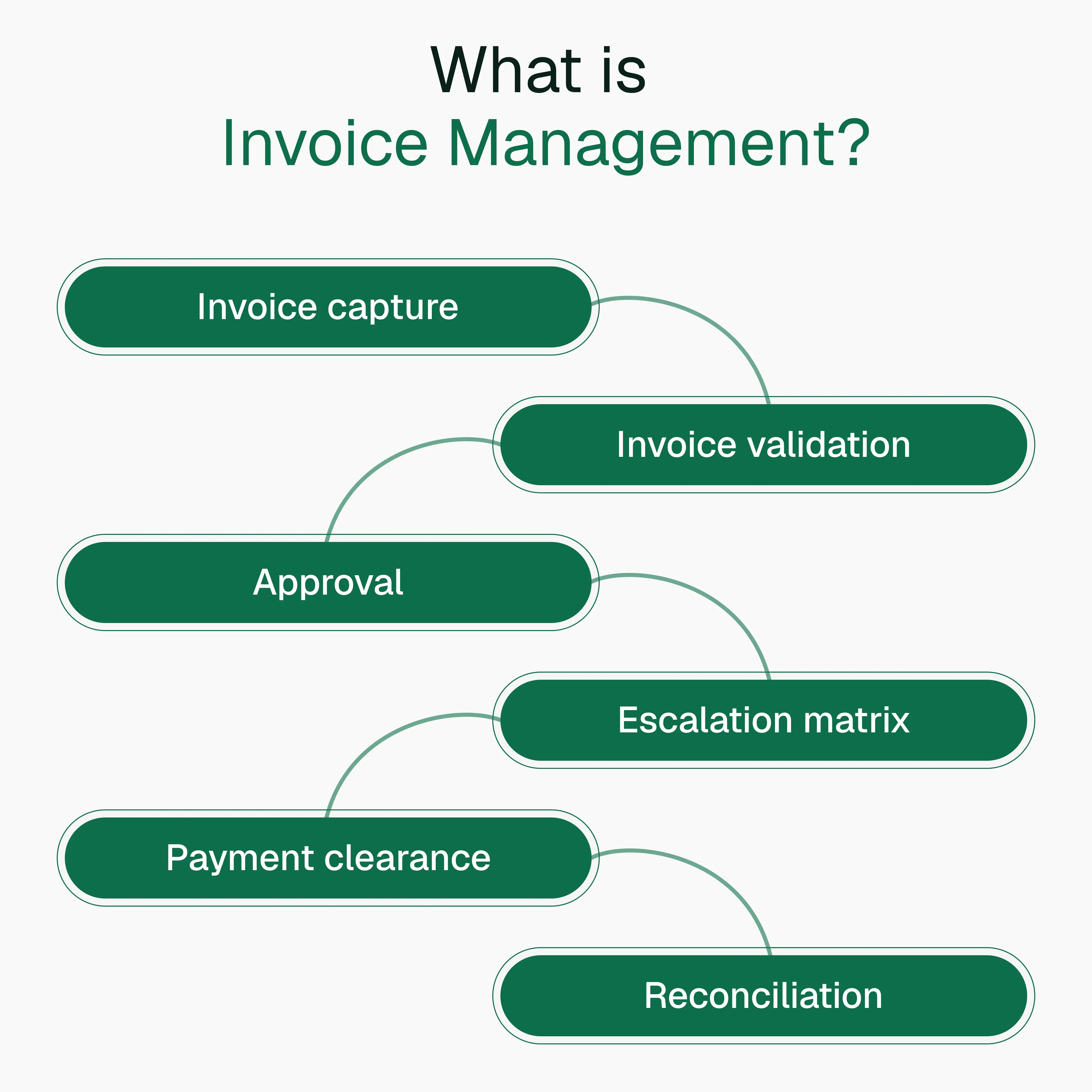

- Invoice approval workflow

In accounts payable, invoices don't just get matched, they need to be approved by team members with the right authorization, after it has been validated for authenticity and accuracy. For smaller companies, it may just be one or two people, for larger enterprises, it may involve a series of approvals from multiple team members.

Setting the right invoice approval workflow ensures that there is neither excess bureaucracy that can stall processing, or too little which can cause errors, frauds or excess payments.

- Vendor invoice

A vendor/ supplier invoice is received by the company in the form of a bill, and is registered as an accounts payable after it has been authenticated. A mere invoice does not account for payable without verification through document matching.

Today, it is standard across industries to receive digital-only invoices, typically via an email record. This is also key to using any accounting or financial software for efficiency and for implementing automation in accounts payable.

- Purchase order (PO)

The purchase order is the primary internal documentation that serves as a tallying document against any vendor invoice. It contains key details of the purchase from a vendor, such as quantity, quality and type of service/ product, vendor’s details etc.

A PO is typically raised by a team lead whose team will use the product or service to be purchased, and is the key verification document used in both 2 way and 3 way record matching when the vendor raised the invoice.

- Good received note (GRN)

A good received note (GRN) is submitted by the team lead/ member who has received goods/ services from a vendor. This is a supporting document used in 3 way matching process, alongside the PO, to validate a vendor invoice.

A GRN is meant to ensure that the quality and quantity of products/ services are as per the requirements in the purchase order. It serves as an added guarantee that no issues took place during the delivery of the items/ services.

This documentation may be simple for companies with small employee strengths, while being elaborative for large enterprises.

- Exception/ error handling protocols

Exception and error handling protocols in accounts payable are a set of rules used to proceed in scenarios where there are exceptional cases or errors. These can be issues with invoice and PO/ GRN mismatch, incomplete or inadequate internal documentation, pricing issues, etc. Every company has their own rules of engagement in such cases with an escalation matrix in place to handle such situations internally and/ or with vendors.

For example, a situation may arise where the invoice and PO data match, but there is a different description in the GRN. In such cases, typically the first line of enquiry is internal investigation with the team that received the goods/ services. If the issue is not resolved and the vendor needs to be contacted, then accounting liaisons with both the internal recipient and the external vendor to resolve the errors.

- Payment process

Once all the mandated validations for a payable has been completed, the payment is processed by the company based on existing financial channels. Today, online transfers are the standard mode of payment, however in certain industries, direct cash or cheque payments are also the norm.

An enterprise should have specific policies detailing in which situations cash/ cheque payments are permitted and the financial trail that needs to be maintained for audit and compliance. This is because online payments have a digital trail that can be easily furnished for external auditors, whereas cash payments require adequate documentation to ensure transparency.

- Reconciliations

Periodic accounts payable reconciliations involve gathering vendor statements and matching that with internal finance ledger to ensure that all transactions and payments have been accurate and error-free. This is a key practice of financial assurance and is typically done quarterly, half-yearly or annually, depending on the volume of transactions in accounts payable.

- Digitization and software

In today’s age, ensuring maximum digitization in accounts payable is critical for scalability, audit and ease. From requesting digital invoice from vendors to ensuring all internal documents are in digital formats, and preferably cloud-based for easy real-time access, and finally, also making payments via online channels as much as possible.

Furthermore, automation platforms like Rever enable accounting teams to process vendor invoices in seconds, with the final results just kept ready for human eyes for a final check. Rever relieves accountants and finance teams from the cumbersome, repetitive and manual tasks of data entry, invoice record matching and reconciliations.

Related: What is Accounting Automation?

Importance of Accounts Payable

- Incorrect billing/ fraud prevention

The accounts payable team is responsible for ensuring that any cash outflow from the company to vendors is accurate and verified. The 2 way/ 3 way record matching process is the cornerstone for this authentication to ensure that bills being sent to the company are genuine and reflect precisely what was ordered and delivered in the form of goods and services.

- Vendor relationship management

Good vendor relations depend on timely payments for delivered goods/ services. Accounts payable team ensures that invoices are processed and cleared within the stipulated time frame as per agreement. The team is also responsible for maintaining proper lines of communications with vendors regarding payments and ensures the right escalation matrix is followed in case of any disputes, for quick and hassle free resolutions.

- Preventing delays and penalties

Enterprises can incur significant penalties for delayed payments due to improper management of vendor invoices, given the size of orders and bills. Accounts payable processes are designed to ensure proper invoice processing and approval workflows, and play a key role in preventing penalty charges by vendors.

- Optimizing subscriptions and usage

Often in enterprise settings, smaller teams or members place subscription order but may not use them efficiently or forget them during employee/ team transitions. Accounts payable ensures that such subscriptions are periodically reviewed and optimized or cancelled depending on existing requirements. This leads to significant cash savings from cutting down unnecessary expenses.

- Audit and compliance

A verifiable data trail for all cash flow with all required details is the cornerstone for healthy auditable accounting books. For all outgoing cashflow to vendors, accounts payable is responsible for maintaining this trail for every transaction.

- Financial projections and reporting

Accounts payable data is a key ledger item that plays into determining the larger financial health of the company. Accurate payables data ensures that financial projections and reports reflect the reality of overall expenses and not get shocked by billings.

Related: What is Expense Management Automation?

Best Practices for Implementing and Managing Accounts Payable in 2026

- Automating repetitive and data-intensive tasks

Tasks such as record extraction, invoice capture and approvals, 2 way/ 3 way record matching, etc can be easily automated using platforms like Rever. Furthermore, such platforms offer rigorous and continuous data authentication, controls and checks to prevent leakages and detect issues at earliest onset.

- Setting clear approval and escalation matrix

Invoice approval workflow is key to ensuring how the vendor invoice circulates and gets approved in an orderly and timely manner. For any exceptions or issues, a clear escalation ladder ensures that the right stakeholders and decision makers are in the chain.

- Periodic review of existing payables

When enterprises conduct a payable review of vendors, needs and usage, often the consolidations pile up to significant amounts in savings. This is especially true for software apps where outdated requirements, redundancies in features and lack of usage run high.

- Ensuring compliance to budget and regulations

Accounts payable is a sensitive function which requires continuous monitoring to ensure it is compliant with regulations and audit-ready at all times. The team is also responsible for ensuring that budget guidelines and limits are adhered and any potential breaches are highlighted and escalated.

- Automation for continuous reconciliation and closure

Sophisticated AI-native finance automation software like Rever enables teams to automate record matching and authentications, approvals and escalations, real-time reconciliations and continuous book closures. This turns close day into a review day for the team, and occurs in real time rather than a weekly or monthly event.